Definition: What is an SPV (Special Purpose Vehicle, also known as Special Purpose Entity)?

A Special Purpose Vehicle (SPV) is a distinct legal entity created by a focunding organization for a narrowly defined financial objective. Its main purpose is to isolate financial risk associated with a specific project, allowing founders to streamline fundraising and investors to pool capital safely.

Special Purpose Vehicle and Special Purpose Entity are synonymous and will be used interchangeably throughout this article.

Summary table: SPV characteristics

Why use an SPV for investment?

From their origins in the 1980s as off-balance-sheet legal structures to isolate financial risk by ring-fencing assets and liabilities from a parent company, the SPV market was valued at approximately $12 billion in 2024 and is projected to grow to $20 billion by 2033 (6.5% CAGR), with 89% of GPs expecting to see growth in SPV deal volumes in 2025.

SPVs offer advantages to each party in an investment transaction, from risk management and deal access for investors to administrative simplicity for founders and strategic flexibility for fund managers.

What’s more, there are also a range of SPV platform providers (like Roundtable in Europe) that can help streamline the SPV creation process to help investors simplify their set up, manage investments and reduce administrative headaches along the way.

SPV Benefits for Investors & Limited Partners (LPs)

For those deploying capital, an SPV offers protection for assets, the ability to pool capital effectively, and access to secondary markets.

- Access and control: An SPV allows investors to pool capital for a single, specific company they choose to back. This is often possible with lower investment minimums making venture capital deals more accessible.

- Financial and tax efficiency: SPVs are typically structured as pass-through entities (like LLCs or LPs), which helps investors avoid double taxation at the entity level. They can be established in tax-friendly jurisdictions such as Luxembourg and The Cayman Islands.

- Cost effectiveness: SPVs generally have lower setup costs and fewer management fees than traditional funds.

- Enhanced liquidity: Depending on the partnership agreement, SPV investors may have the right to sell their stakes to other shareholders or third parties, providing more opportunities to realize returns.

SPV Benefits for Founders & Target Companies

For the companies receiving capital, the primary advantage of an SPV is operational simplicity and a cleaner path to future growth.

- Simplified capitalization table: An SPV for founders makes it simple to accept capital from a large group of individual investors while only adding a single line item to their capitalization (cap) table.

- Streamlined administration: The company can share information with one SPV instead of many individual investors, reducing the reporting burden.”.

SPV Benefits for Fund Managers, GPs & Syndicate Leads

For those organizing investments, SPVs are a flexible instrument for building a track record, executing strategy, and creating economic incentives.

- Build a track record: Raising capital via a deal-by-deal SPV is often faster and easier than raising a traditional blind-pool fund, including for emerging managers and syndicate leads.

- Strategic & opportunistic investing: SPVs give fund managers flexibility. They can be used to pursue compelling opportunities that fall outside a main fund's specific thesis or concentration limits. They also allow managers to exercise pro-rata rights to make follow-on investments in successful portfolio companies, even when the primary fund lacks the capital to do so. Finally, they can be used as "continuation funds" to hold onto a winning asset beyond a fund's original lifecycle.

- Economic alignment: The SPV structure allows the organizer or syndicate lead to earn carried interest, a share of the profits from the investment, aligning their financial success with that of their investors.

What are the different types of SPV?

While all SPVs share core characteristics like legal separation and a limited purpose, they can be categorized into four primary types based on their function.

Investment vehicles

As an Investment Vehicle, an SPV’s primary role is to pool capital from multiple investors to make a targeted investment. This structure is central to modern alternative investing.

- This is the standard for venture capital deals, angel syndicates, and opportunistic "sidecar" investments. SPVs are also used for securitizing loans, facilitating co-investments, and creating SPACs as a faster alternative to a traditional IPO.

- They provide investors with deal-by-deal choice, democratize access with lower investment minimums, and allow fund managers to pursue flexible strategies.

Looking to set up an investment vehicle?

Roundtable makes it easy to launch and manage SPVs, from onboarding investors to handling legal, KYC, and ongoing administration. Get your deal live in days, with full control and transparency.

Project companies

This type of SPV is created to execute a specific, large-scale, and often collaborative endeavor. It functions as the legal and operational entity for a single project, containing all related activities and financing.

- Project Companies are integral to public-private partnerships (PPPs) for capital-intensive infrastructure, used to manage real estate developments, and formed as joint ventures for companies to collaborate on new products without a full merger.

- They allow partners to share and absorb risk while streamlining project-specific financing and management.

Intermediate SPVs

An Intermediate SPV functions as a "middleman" entity, designed to own specific assets and legally separate them from the parent company for risk protection and transactional efficiency.

- This structure is used to create a "bankruptcy-remote" shield for assets, hold individual real estate parcels to isolate liability, and simplify asset transfers by packaging an asset and its permits into a single, sellable entity. They are also frequently used in Leveraged Buyouts (LBOs) to house acquisition debt.

- They offer robust liability protection and risk isolation, ensuring that the financial distress of one asset or entity does not impact the broader portfolio or parent company.

Jurisdictional Shell Companies

This type of SPV is strategically established in a specific legal or tax jurisdiction to leverage benefits related to tax treatment, privacy, or regulatory compliance.

- They are often registered in tax-friendly jurisdictions to optimize financial outcomes. Their main advantages are tax efficiency and simplified compliance for international or tax-sensitive investors.

- Note, SPVs are often scrutinized by tax authorities, so careful consideration and involvement of legal specialists are required to ensure that all structures are compliant.

Note on SPV vs. regular subsidiary

All SPVs may be subsidiaries, but not all subsidiaries are SPVs.

An SPV is distinguished by its limited purpose, operational autonomy, and often special structural features (e.g., minimal equity, independent governance), designed to achieve off-balance-sheet treatment, subject to IFRS 10 and ASC 810 consolidation tests.

What are use cases for an SPV?

The fundamental characteristics of an SPV make it a versatile tool for transactions in a range of industries.

SPVs for Venture Capital & Private Equity

In private markets, SPVs for venture capital deals help structure investments, pool capital, and manage risk on a deal-by-deal basis.

- Targeted investing: SPVs allow investors (LPs) and angel syndicates to pool capital for a single, specific company, rather than investing in a broad fund portfolio. This provides direct choice and visibility over the investment.

- Greater access: The structure often allows for lower investment minimums, making high-growth startups accessible to a wider range of investors. For angel groups, it allows them to write larger checks and negotiate better deal terms.

- Strategic fund management: For fund managers (GPs), SPVs are used to make opportunistic "sidecar" investments outside a fund’s core thesis, execute follow-on investments to support winning companies, and build a track record before raising a traditional fund.

- Founder simplicity: For founders receiving investment, an SPV consolidates many small investors into a single entity on their cap table, dramatically reducing administrative work.

Fund faster with Roundtable

Move your deals forward with confidence, backed by Roundtable’s digital SPV creation platform. Let us handle everything from legal setup to LP management while you do what you do best – make deals happen.

Find out more about our SPVs for Venture Capital and Private Equity

SPVs for Real Estate & Property Management

SPVs are a common occurrence in modern real estate investment, used to finance, own, and manage properties with greater efficiency and protection.

- Liability isolation: By placing each property into a separate SPV, owners can isolate liabilities. A legal claim or financial issue related to one property will not affect others in the portfolio.

- Tax optimization: SPVs can offer significant tax advantages. Instead of selling a property and incurring high property sales tax, the owner can sell the SPV that holds it, often resulting in a lower capital gains tax bill.

- Improved financing: An SPV holding a valuable property can often secure better loan terms based on that asset's value, without impacting the parent company's creditworthiness.

SPVs for Securitization & Structured Finance

Securitization relies on SPVs to transform illiquid assets into tradable securities.

- A financial institution, such as a bank, sells a pool of assets (like mortgages, loans, or receivables) to an SPV.

- The SPV then issues tradable, asset-backed securities to investors.

- Because the assets are isolated in the bankruptcy-remote SPV, investors are shielded from the bank's own financial health, and their claim is tied directly to the performance of the underlying assets.

SPVs for Mergers, Acquisitions & IPOs

SPVs provide flexible structures for facilitating complex corporate finance transactions, including M&A and public offerings.

- Facilitating M&A: SPVs can be used as intervening entities to solve structural problems when one company acquires another, such as a C-corporation acquiring an S-corporation.

- "Up-C" for IPOs: When a privately-held partnership goes public, it can use a C-corporation SPV to hold the partnership interests, which then undertakes the IPO.

- SPACs: A Special Purpose Acquisition Company (SPAC) is a type of SPV created specifically to raise capital through an IPO in order to acquire an existing private company, offering a faster alternative to a traditional IPO process.

Public-Private Partnerships (PPPs)

SPVs are a common part of public-private partnerships, especially for large-scale, capital-intensive infrastructure projects common throughout Europe. The SPV structure is often demanded by the private sector partners to help absorb and manage the significant financial risks involved in such long-term projects.

How does an SPV compare to other business structures

SPV vs SPAC

While a Special Purpose Acquisition Company (SPAC) is a specialized type of SPV, their distinct goals lead to very different structures and operations.

SPV vs Investment Fund

While both are vehicles for investment, an SPV's structure and purpose differ significantly from that of a traditional investment fund, such as a venture capital or private equity fund. An SPV offers a targeted, single-deal approach with greater investor discretion, whereas a fund provides a long-term, diversified portfolio managed by a General Partner (GP).

Advantages of an SPV

By design, an SPV provides a framework for isolating risk, optimizing financial outcomes, and creating flexible, tailored investment opportunities for investors, founders, and fund managers alike.

- Risk isolation and liability protection: An SPV's primary advantage is shielding the parent company or main fund from the financial risks and legal liabilities of a specific project. Because it is a "bankruptcy-remote entity," its operations can continue even if the parent company faces insolvency, making it ideal for high-stakes ventures.

- Tax strategy: SPVs can provide tax benefits, often through a pass-through structure that avoids double taxation at the entity level. They can be used strategically to minimize tax on specific transactions, such as property sales, and can be established in favorable jurisdictions to reduce overall tax burdens.

- Investor access and control: For investors, SPVs offer visibility and active decision-making on a deal-by-deal basis, a level of control not typically found in traditional funds. The structure also enables lower investment minimums, making alternative assets accessible to a broader range of investors.

- Strategic benefits for founders and GPs: Founders benefit from a simplified cap table, as multiple investors are consolidated into a single entity. For emerging fund managers (GPs), SPVs are an effective tool for building an investment track record before raising a larger, traditional fund.

- Financial and operational efficiency: The SPV structure streamlines complex transactions like project financing or asset transfers, reducing administrative workload. It can improve access to capital and help secure better financing terms by isolating specific assets.

Compared to traditional funds, SPVs are often quicker and more cost-effective to set up and maintain, especially when working with a specialised partner like Roundtable.

Get moving faster

Get your SPV live without the legwork with Roundtable’s complete digital platform. We handle everything from entity formation to investor onboarding and KYC, as well as drafting tailored legal agreements that fit your deal, so you can focus on closing investments.

Find out more by talking to one of our experts.

Disadvantages of an SPV

While useful, SPVs come with their own specific challenges, from their inherent complexity and operational costs to the potential for regulatory changes and misuse.

- Complexity and opacity: SPV structures can be highly intricate, making it difficult for investors and even sponsors to fully comprehend the underlying financial risks. This complexity can lead to a lack of transparency and challenges in accurately valuing the assets held by the vehicle, placing a significant due diligence burden on all parties.

- Regulatory scrutiny: The features that make SPVs useful, such as legal separation and opacity, can be exploited. Historically, they have been misused in high-profile cases to hide debt and inflate earnings. They can also be used in aggressive international structures for tax avoidance, which has led to increased scrutiny from global bodies.

- Operational and counterparty risks: Setting up and managing an SPV involves significant costs, time, and administrative effort. The vehicle is also dependent on external parties like servicers and administrators; the failure of any key counterparty can disrupt cash flows and create significant operational or market risks.

- Regulatory risk: SPVs are vulnerable to changes in the legal and financial landscape. New accounting standards, evolving tax laws (like BEPS initiatives), or stricter financial regulations (like AIFMD) can impose new costs and compliance burdens, potentially altering an SPV’s financial viability overnight

How does an SPV work?

SPV Core Concepts

- Separate legal personality: An SPV has its own legal status, distinct from its creator. It owns its own assets, incurs liabilities, enters into contracts, and maintains a separate balance sheet, a feature that is fundamental to its operation.

- Limited purpose: An SPV is a "fenced organisation" created for a singular, specific purpose. Its governing documents strictly limit its activities to a predefined objective, such as holding a particular asset, which prevents it from taking on unrelated debts or business lines.

- Bankruptcy remoteness: A primary goal of the structure is to make the SPV "bankruptcy-remote". This insulates the SPV’s assets from its parent’s creditors in case of insolvency, and vice versa. Note: "remote" does not mean "immune" – a court can still challenge the SPV's separation from its parent in exceptional circumstances.

- Custom capital structure: To enhance its independence, an SPV often has a custom capital structure with minimal equity. In an "orphan" structure, ownership can be held by an independent third party, like a trustee, instead of the sponsor.

- Defined lifespan: Many SPVs are designed to be temporary, dissolving once their specific purpose is fulfilled, such as when a project is completed or a financing is repaid. Others may be ongoing but remain strictly limited to their original venture.

Common legal forms of SPVs

An SPV is not a single, rigid structure – it can be established in a variety of legal forms, with structures to be found in major financial jurisdictions across the US, Europe, and offshore centers.

For more information on SPV forms by region, see the section below.

Key players in an SPV

A successful SPV relies on a network of participants, each performing a specific role to ensure the vehicle is structured, funded, and managed effectively.

- Sponsor (or parent company): This is the organization that creates the SPV. Its primary motivation is to isolate the financial risk of a specific project from its own balance sheet.

- Investors (or Limited Partners): Individuals or firms who provide capital to the SPV in exchange for an equity stake. Their goal is to gain targeted exposure to a specific investment opportunity, often with lower minimums and more deal-by-deal control than a traditional fund offers.

- Manager (GP or Syndicate Lead): The manager is the individual or firm that sources the deal, organizes the SPV, and manages it on behalf of investors. They are responsible for all operational aspects, from investment decisions to investor reporting, and are compensated through management fees and carried interest (a share of the profits).

- Target company: The company that receives the investment from the SPV. For founders, the primary benefit is a simplified capitalization table, as the SPV consolidates many individual investors into a single line item, reducing administrative work.

- Service providers: A network of professionals provides essential support. This includes law firms for legal structuring, accountants for tax and financial reporting, banks for holding funds, and specialized SPV administrators for back-office management and compliance.

- Regulators: Government agencies (like the SEC in the US) set the legal framework for SPVs. They enforce securities and tax laws and often place limits on the number and type of investors who can participate in an offering.

Legal forms for SPVs by country

SPVs in the United States

The US offers a highly developed and flexible environment for SPVs, with Delaware being the favored state of incorporation for its robust corporate law. The choice of entity is typically driven by the need to balance strong liability protection with pass-through tax efficiency.

Key structures include:

- Limited Liability Company (LLC): The most popular choice for venture capital, real estate, and private equity SPVs, offering high contractual flexibility.

- Limited Partnership (LP): A prevalent structure for investment funds and international deals, providing limited liability to investors.

- Trusts and Corporations: Used for more niche purposes, such as securitizations (Trusts) or as "blocker" entities for tax-sensitive investors (C-corps).

Regulation is primarily overseen by the SEC. SPVs must comply with securities laws, which often restrict the number of investors and require them to be "accredited investors".

SPVs in the United Kingdom

The UK provides several distinct legal structures for SPVs, ranging from traditional corporate forms to more tax-transparent partnership and trust arrangements.

Key structures include:

- Private Limited Company (Ltd): The most frequent SPV form, providing limited liability but subject to UK Corporation Tax and more compliance than US LLCs.

- Private Fund Limited Partnership (PFLP): A common tax-transparent choice for UK venture capital SPVs, though it requires a regulated manager and has higher administrative costs.

- Bare Trust: A simple, low-cost nominee structure where the trustee holds shares for beneficiaries. It is tax-transparent and often used as an unregulated alternative to partnership. It’s also the only type of UK SPV which allows investors to benefit from EIS, SEIS tax relief schemes, providing additional tax reliefs.

SPVs in France

In France, SPVs can be structured using a range of corporate and partnership vehicles, with a growing preference for more flexible corporate forms. France also has highly specialized, bankruptcy-remote vehicles for securitization.

Key structures include:

- Société par Actions Simplifiée (SAS): An increasingly popular and flexible corporate form offering limited liability and significant freedom in governance.

- Société Civile (SC): A tax-translucid partnership (taxed at investor level, rather than company level) commonly used for real estate, though partners face unlimited liability for the entity's obligations.

- Organisme de Titrisation (OT): A specialized, tax-efficient vehicle for securitization. In its fund form (FCT), it has no legal personality but is bankruptcy-remote by statute.

SAS vs SC for SPVs

Roundtable offers both Société par Actions Simplifiée (SAS) and Société Civile (SC) as primary SPV structures in France due to their tax-translucent nature, meaning the SPV itself is not taxed at the corporate level.

Instead, profits and capital gains are taxed once, directly in the hands of investors, according to their personal tax regime. This structure avoids the double taxation often found in standard corporate entities, so in most cases investors can retain a larger share of net returns.

Read more about French SPV taxation

SPVs in Germany

Germany's SPV landscape is characterized by well-defined corporate and partnership structures, with a focus on providing strong limited liability (Haftungsbeschränkung).

Key structures include:

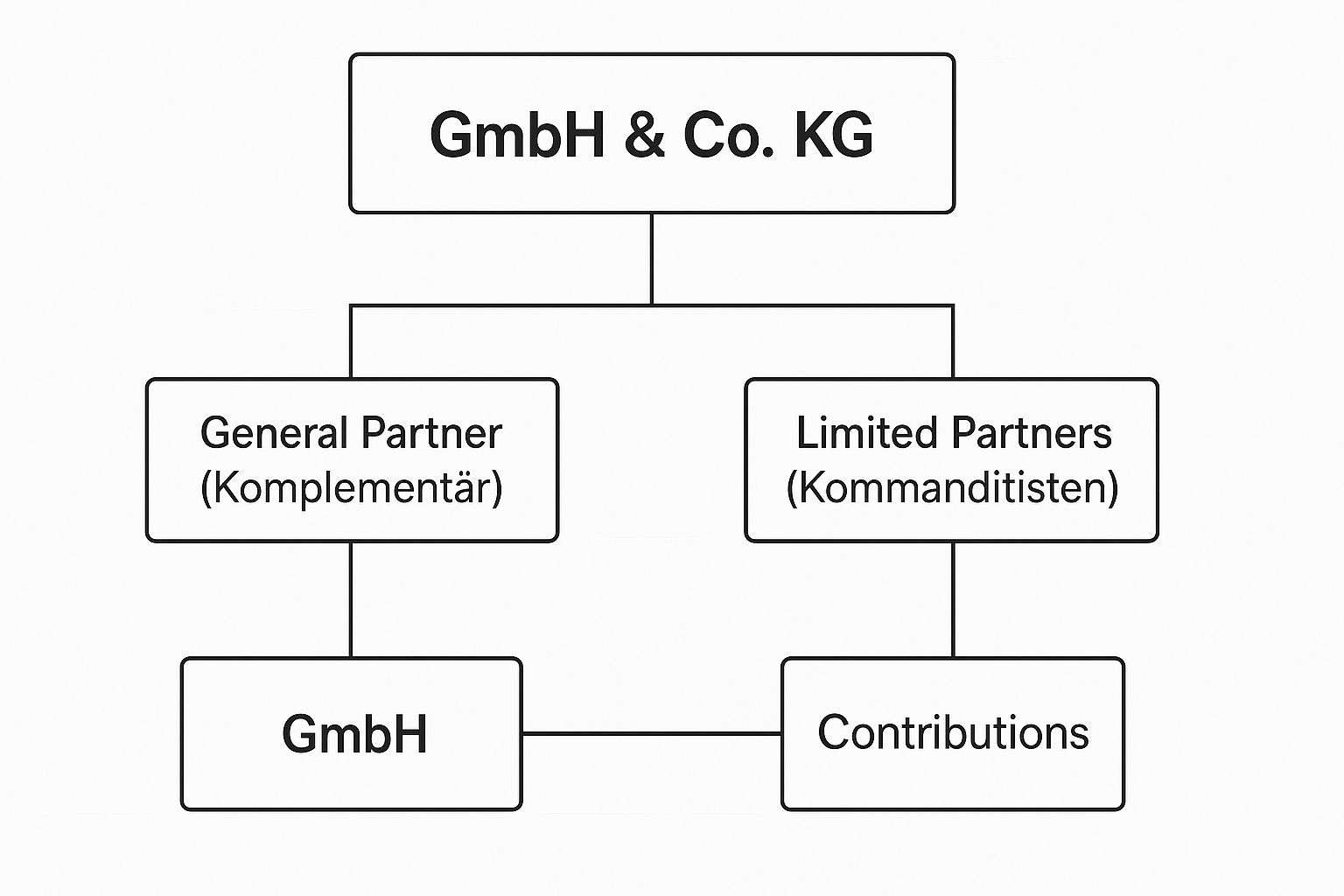

- Gesellschaft mit beschränkter Haftung (GmbH): The most common form for a project-specific SPV (Projektgesellschaft), it provides limited liability but is subject to corporate tax and requires a minimum capital of €25,000.

- GmbH & Co. KG: A popular limited partnership that uses a GmbH as the general partner. This structure achieves overall limited liability while retaining the pass-through tax treatment of a partnership.

SPVs in Luxembourg

As a major European financial hub, Luxembourg offers a diverse range of SPV structures favored for holding companies and alternative investment funds due to their flexibility and tax efficiency, with access to European markets.

Key structures include:

- Société à responsabilité limitée (SARL): The most common form used for investment SPVs and holding companies, offering limited liability with a minimum capital of €12,000.

- Société en commandite spéciale (SCSp): A highly flexible special limited partnership that has no legal personality. It is fully tax-transparent and increasingly popular for alternative investment funds.

- SCS and SCA: The Société en commandite simple (SCS) is a tax-transparent limited partnership, while the Société en commandite par actions (SCA) is a partnership limited by shares, combining corporate and partnership features.

Launch your Luxembourg SCSp with Roundtable

The SCSp is Luxembourg’s most flexible and tax-efficient SPV structure, combining contractual freedom, investor privacy, and EU-wide market access.

Roundtable makes it simple to set up and manage your SCSp by handling incorporation, bank accounts, investor onboarding (KYC/AML), and ongoing administration on a single platform.

Find out how you can get your SCSP off the ground faster.

SPVs in Spain

In Spain, the Special Purpose Vehicle (SPV) is a common tool for foreign investors, typically established as a subsidiary of a foreign company. Its structure is designed to secure assets and isolate the Spanish entity from any financial distress affecting the parent company, with a primary focus on securitization transactions.

Key structures used for SPVs in Spain include:

- Sociedad Anónima (S.A.): The equivalent of a corporation, this structure is typically used for large or complex securitization transactions involving a high number of assets.

- Sociedad de Responsabilidad Limitada (S.L.): Similar to an LLC, this form is generally used for transactions involving a smaller number of assets.

- Fideicomiso (Trust): A very common SPV structure in which assets are held in a trust that issues securities directly to investors.

SPV structure comparison table by region

Accounting, tax and regulatory considerations for SPV

Setting up an SPV requires taking into account a range of tax, accounting, and regulatory considerations. These rules vary significantly by jurisdiction and structure.

Making the right, strategic choices requires careful planning and expert guidance to ensure the vehicle achieves its intended purpose without creating liabilities.

Tax considerations for SPVs

The tax treatment of an SPV is a primary driver of its structure but also a source of significant risk if not handled correctly.

- Entity taxation: The default tax status of the SPV is a foundational choice. Many SPVs in the are structured as pass-through entities (like SC or SCSp), where the entity is not taxed directly, but investors are.

- Jurisdiction: The choice of jurisdiction can have major tax consequences. SPVs are often established in tax-friendly locations, but this requires careful planning to manage withholding taxes and international reporting requirements like FATCA.

- Transactional taxes: Specific transactions, such as selling property held within an SPV, can be structured for tax optimization, but these strategies require domain expertise to execute correctly.

Accounting & reporting for SPVs

Proper accounting is crucial for transparency and avoiding the misuse of SPVs, as seen in historic corporate scandals. Maintaining a clear and compliant financial picture is a critical, ongoing task.

- Separate financials: An SPV must maintain its own distinct books, records, assets, and liabilities, separate from the sponsor.

- Off-Balance sheet treatment: While SPVs may be kept off a sponsor's balance sheet, this practice is now under stricter scrutiny and requires careful disclosure to avoid masking crucial information from investors.

- Expense allocation: Regulators like the CSSF and AFM have made the proper allocation of expenses between the SPV and its managers an examination priority, with significant fines for non-compliance.

Legal & regulatory framework

SPVs do not operate in a vacuum; they are subject to a web of requirements that dictate their formation and operation. These can be understood across three main dimensions:

1. Regulatory

- Securities laws: In most jurisdictions, SPVs that issue securities must comply with strict regulations (like Law No. 88-121 in France) regarding how they can raise capital and who can invest.

- Investor limitations: Offerings are often restricted to accredited or otherwise sophisticated investors, and there may be limits on the number of investors permitted.

- Ongoing compliance: Regulators also require continuous filings, such as KYC/AML checks, state franchise taxes, registered agent fees, and other disclosures.

2. Corporate

- Legal structure: The choice of entity (e.g. SAS, SC, SCSp) dictates governance rules, liability, and reporting requirements. This decision shapes both how the SPV operates internally and how it is treated by regulators.

3. Fiscal

- Tax treatment: SPVs are often designed to be tax-transparent, ensuring that profits and capital gains are only taxed once at the investor level. However, treatment can vary significantly across jurisdictions, so cross-border investors must consider the fiscal implications in each relevant country.

The sheer number of variables makes professional support essential. Platforms like Roundtable are designed to manage these requirements, handling the legal, tax, and administrative burdens so that founders and investors can focus on the deal itself.

Simplify SPV compliance with Roundtable

Roundtable handles the KYC and AML requirements of your European SPV, with centralized administration through our platform, from formation to ongoing administration, so you stay fully compliant.

Find out more by talking to one of our experts.

SPV best practices

A robust SPV should always be designed with support from experienced legal, tax, and administrative professionals, the below best practices should be considered a starting point.

- Legal and structural soundness: An SPV’s constitutional documents should enforce a narrow, limited purpose to prevent unforeseen liabilities. The choice of jurisdiction is critical and should be based on investor familiarity and legal precedent, not just tax rates.

- Robust contractual framework: Consider embedding "non-petition" and "limited-recourse" language in all contracts to prevent creditors from filing for bankruptcy against the SPV. From day one, the legal agreements should clearly document exit mechanics, payment waterfalls, and wind-down procedures to avoid future deadlocks.

- Operational integrity: Maintain strict operational separation from the sponsor, with separate bank accounts, books, and records. Where possible, automate back-office processes using integrated platforms to manage costs and administrative work effectively.

- Transparent reporting and compliance: Establish a fixed timetable for audited, investor-grade reporting. It is essential to implement strict AML/KYC workflows for all investors and continuously track evolving regulations, such as SEC and EU rules, to ensure ongoing compliance.

- Proactive risk management: Before launch, secure legal opinions confirming the SPV's bankruptcy-remote status. A living risk playbook should be embedded from the start, mapping all counterparties and running stress tests to pre-agree on remedial actions for potential crises.

SPV Risks and challenges

Even a correctly structured SPV presents challenges that require diligent management. Especially when it comes to tax, accounting, and regulation, where the obligations are continuous and the penalties for non-compliance can be severe.

SPV tax risks

SPVs create specific cross-border and compliance risks that can impact investor returns if not managed proactively.

- Withholding tax: In cross-border structures, there is a significant risk that withholding taxes could be levied at multiple levels, both between the startup and the SPV, and between the SPV and its investors, which can significantly reduce net returns.

- International reporting: Using offshore SPVs can trigger complex U.S. reporting requirements for American investors, such as those under the Foreign Account Tax Compliance Act (FATCA) and controlled foreign corporation (CFC) rules.

- Compliance burden: Each SPV must obtain its own Tax Identification Number (TIN) and is typically required to file its own federal and state income tax returns, adding a layer of administrative complexity.

Accounting and reporting challenges

The financial separation that makes SPVs useful also creates accounting challenges, demanding transparency and rigorous oversight to prevent misuse.

- Potential for obscuring financials: Historically, SPVs have been misused to hide corporate debt and fabricate earnings. This risk requires investors to conduct thorough due diligence on the financials of both the SPV and its sponsor, not just one or the other.

- Scrutiny on expense allocation: Regulators like the SEC are increasingly focused on how expenses are allocated between the SPV and its managers. Incorrectly charging certain costs to the SPV can lead to regulatory fines.

- Maintaining separate records: While essential for compliance, maintaining a complete and accurate set of books and records that is separate from the sponsor is a significant ongoing operational challenge.

Regulatory and governance risks

SPVs operate within a strict and varied regulatory framework, creating risks related to compliance, investor rights, and governance.

- Investor limitations: Regulations in jurisdictions like the U.S. impose firm limits on the number and type of investors an SPV can accept, with most offerings restricted to "accredited investors".

- Limited investor rights: LPs in an SPV typically have no direct voting or information rights in the underlying company. Their legal relationship is with the SPV manager, who holds the official shareholder position.

- Incentive misalignment: A potential conflict can arise if a manager earns carried interest on an SPV deal without investing their main fund's capital, meaning the LPs bear the primary financial risk.

- Ongoing compliance burden: SPVs are subject to continuous compliance obligations, including state-specific franchise taxes, registered agent fees, and securities filings, all of which carry penalties for failure.

Roundtable SPVs are deal-specific vehicles that do not qualify as Alternative Investment Funds (AIFs) and are not subject to fund regulations. They are generally tax-transparent, with taxation occurring at the investor level. Individual tax and legal consequences may vary; investors should seek independent advice.

Common SPV pitfalls

The complexity of SPVs creates opportunities for mistakes.

Flaws in the legal structure, financial mismanagement, or compliance gaps can undermine the vehicle's purpose, leading to financial loss or regulatory penalties.

Structural & legal flaws

- Imperfect asset transfer: If an asset transfer is not structured as an airtight "true sale," courts may pull the assets back into the sponsor's estate, voiding the SPV's protections.

- Weak separateness: Commingling cash or using shared stationery can lead regulators to conclude the SPV is not truly separate, collapsing its legal structure.

- Lack of independent veto: Without a neutral director required to approve an insolvency filing, the sponsor could unilaterally file for the SPV's bankruptcy.

- Implicit sponsor support: Any back-door promise of support or guarantees from the sponsor can undermine the SPV's financial independence and risk isolation.

Financial & operational pitfalls

- Opaque investor disclosures: Failing to be fully transparent about underlying assets, fees, and side letters can lead to a loss of investor confidence and potential liabilities.

- Over-leverage: Taking on too much debt or mismatching liabilities can create servicing shortfalls during amortization.

- Hidden costs: Under-scoping the budget for the full lifecycle of admin, audit, and tax fees will ultimately erode net investor returns.

- Inaccurate timelines: Underestimating the time required for essentials like investor KYC and bank account opening can cause critical funding delays or bridge-funding costs.

- Forgotten exit plan: Having no clear plan or funds reserved for the wind-down phase can create a "zombie" entity that incurs unnecessary taxes and fees.

Governance & compliance issues

- Conflicts of interest: When a sponsor also acts as the asset manager without proper firewalls, it can lead to misaligned incentives and asset quality drift.

- Compliance gaps: Failures in KYC/AML and investor accreditation workflows can result in funding delays and significant regulatory fines.

- Waterfall & payment errors: Mis-allocating funds during distributions can force costly restatements and damage credibility with investors.

SPV Case Studies

SPVs are now a common part of the investing landscape, with funds using SPVs to manage exposure to emerging fields and companies.

SPVs for founders case study: Pletor's strategic angel round

For its €1.5 million first fundraising round, AI startup Pletor needed to bring in a diverse group of international angel investors who could provide deep expertise in marketing, design, and AI.

- The challenge: The founders wanted to onboard a dozen strategic angels from France, Germany, the UK, and Spain. They knew that managing this process individually would create significant administrative and legal hassles, distracting them from the core business of building their company.

- The SPV solution: Pletor used Roundtable to create a single SPV to pool all of their angel investors. This allowed the founders to easily track commitments and streamlined the entire process for their investors, who could onboard and sign all documents digitally on a single platform.

- The result: By using an SPV, Pletor successfully brought in high-value strategic investors without the administrative workload. The founders maintained a clean cap table and were able to focus on investor engagement and scaling their business, rather than managing paperwork.

Read more about Pletor’s SVP strategy

SPVs for investment clubs case study: scaling Super Capital

Super Capital, a French investment community with over 1,000 active members, uses SPVs to structure their early-stage tech investments and scale their operations.

- The Challenge: Super Capital wanted to grow its community and increase its average investment size to have a more significant impact on a startup's cap table. They needed a platform to manage a large, diverse group of investors and streamline their deal-by-deal investment process.

- The SPV Solution: The firm uses Roundtable to create SPVs for specific deals, allowing them to offer opportunities to their community even if the deal doesn't fit the thesis of their main collective vehicle. This provides flexibility and allows individual members to opt into deals they are passionate about.

- The Result: By using Roundtable's SPV structure, Super Capital can manage its large community, organize deal-by-deal investments efficiently, and aim to triple its typical deal size from ~€100k to over €300k. The platform gives them the visibility and structure needed to professionalize their community-led investment model.

Learn more about Super Capital’s SPVs for investment clubs approach

SPVs for fund managers case study: Better Angle's flexible syndicate model

Better Angle, a French community-led investment firm, uses a deal-by-deal SPV model alongside its flagship funds to enhance flexibility and provide more opportunities for its network of over 200 entrepreneurs.

- The challenge: The firm wanted to invest in specialized or sensitive sectors, like defense tech, that didn't align with the values of their broader investor community. They also wanted to give their existing LPs a way to increase their exposure to high-performing companies in the main fund.

- The SPV solution: Better Angle uses Roundtable to launch deal-by-deal SPV syndicates. This allows interested investors to opt into specialized deals without affecting the core funds. It also enables their fund LPs to "double down" on specific opportunities they are passionate about.

- The result: Roundtable's platform handles the operational load for these syndicates, from investor onboarding and KYC to compliance. This gives Better Angle the flexibility to offer tailored deals, engage their community, and close investments much faster, averaging three deals a month.

Read more about Better Angle’s SPV model for syndicates

SPV for international angels case study: Pruna AI’s global alignment

For its $6.5 million seed round, German-French startup Pruna AI used a Roundtable SPV to bring in strategic angel investors from across the globe.

- The challenge: The founders needed to onboard about a dozen strategic angels from multiple countries, but were warned that managing this individually would be a logistical "nightmare" due to Germany's bureaucratic fundraising process.

- The SPV solution: They used Roundtable to create a single, Luxembourg-based SPV to consolidate all international investors. This streamlined the relevant cross-border paperwork and simplified the entire process.

- The result: The SPV delivered a faster, smoother, and more efficient fundraising experience for the Pruna AI team, their lawyers, and their angels. By handling the administrative hassle, Roundtable enabled the founders to focus on selecting the right strategic partners to help them scale.

Read more about Pruna’s angel syndicate SPV

How to setup your SPV

Setting up an SPV requires a strategic set of choices – from where to incorporate to how to structure capital and shares – that can influence the success of your investment and your potential returns. Key steps to understand are:

- Pre-formation planning

Before any legal documents are filed, the foundation of the SPV dictates all future steps.

Key strategic decisions include:

- Define sponsor goals: The process begins by clearly defining the SPV’s purpose, whether it's for risk isolation, securitization, a joint venture, or tax optimization. This goal dictates the entire structure.

- Select a jurisdiction: The choice of jurisdiction is critical. Key criteria include the speed of formation, a court system with a strong track record on insolvency remoteness, and familiarity to target investors.

- Ensure economic substance: To comply with modern tax regulations like BEPS 2.0, the SPV must have genuine economic activity. This may require local directors and robust independent governance to maintain its legal and tax separation.

Roundtable perspective: Investment is increasingly borderless – if you’re eyeing cross-border deals, make sure you’re working in a region that can access funds from multiple jurisdictions.

Roundtable specializes in standardized, compliant SPV structures in leading European jurisdictions like Luxembourg and France, that offer the right combination of flexibility and tax efficiency.

- Legal formation and structuring

This phase involves legally creating the entity and establishing its operational rules. The key mechanics are:

- Choose a legal entity: Select the appropriate legal form, such as a Limited Liability Company (LLC), Limited Partnership (LP), or a corporate entity held in an "orphan" trust structure.

- Draft governance documents: Create core legal agreements like the Memorandum and Articles of Association or Partnership Agreement. These define the SPV's constitution, powers, and internal rules. (This is where an experienced partner like Roundtable can help reduce risk and uncertainty).

- File and appoint: File the necessary formation documents with the jurisdictional authority, appoint a Registered Agent, and obtain a Tax ID Number.

- Engage service providers: Assemble a network of crucial partners, including legal counsel, tax advisors, a trustee to represent investors, a servicer to manage assets, and an SPV administrator for day-to-day operations.

Roundtable perspective: For investors and founders, this stage is often the most time-consuming, and has the potential to slow down the deal or hinder future negotiations if drafting is not done with an eye to the future.

An end-to-end platform like Roundtable replaces the need to coordinate multiple service providers by handling the entire legal formation, document drafting, and administrative setup for you.

- Capitalization and funding

With the legal entity in place, the SPV is funded and receives the assets it was created to hold.

- Asset transfer: The core assets are transferred to the SPV via a "true sale", a transaction structured to be robust against the originator’s potential insolvency.

- Raise funds: The SPV raises capital by issuing securities, such as notes, bonds, or certificates, to investors, which are backed by the SPV's assets.

- Define the waterfall: Transaction documents must meticulously define the cash flow waterfall, outlining the priority of payments: first operational fees, then interest and principal to investors (often by tranche), and finally residual profit.

Roundtable perspective: Winning investors is only half the battle – robust due diligence and compliance are key to safeguard your investment and make future management simpler.

Roundtable automates investor onboarding, KYC/AML checks, digital document signing, and secure fund collection, allowing you to close your round faster.

- Plan for operation and exit

A successful setup includes planning for the entire lifecycle of the vehicle, from its daily operations to its eventual dissolution.

- Ongoing administration: Plan for ongoing tasks, including investor reporting (on NAV, IRR, etc.), regulatory reporting (e.g., beneficial ownership updates), and tax reporting (e.g., FATCA/CRS).

- Exit and dissolution: The governing documents must specify dissolution triggers (e.g., project completion, asset sale, or investor vote) and the wind-down process, which includes settling all debts, filing a dissolution certificate, and making a final distribution of any residual assets.

Roundtable perspective: Once you’ve made your investment, ongoing reporting and compliance can be a major drain on resources without the right tools.

Roundtable’s platform centralizes these tasks, handling everything from investor updates and tax documentation to the final distribution and dissolution of the vehicle.

How to set up an SPV with Roundtable in Europe

Roundtable’s platform helps you automate the complexities of creating and managing a SPV so you can focus on finding investors and making deals happen.

Our streamlined experience helps dealmakers to launch their SPV quickly to capitalize on opportunities and provide the best investor experience possible.

Roundtable's all-in-one platform covers the end-to-end process of creating and managing your SPV, including:

- Automated setup: The platform handles the entire incorporation process, from registering the vehicle in key jurisdictions to setting up the required bank accounts.

- Digital investor onboarding: A digital workflow covers the full investor onboarding process, including all Know-Your-Customer (KYC) checks, to ensure compliance and a smooth investor experience.

- Centralized governance: Roundtable acts as the SPV manager, creating and housing all necessary legal documents and contracts on the platform. Key governance actions, such as investor voting, are managed digitally.

- Secure transaction management: The entire investment process is managed on the platform, from the secure digital signing of agreements to the efficient collection and deployment of funds.

Find out how you can get started today by talking to one of our experts.

What’s the best SPV platform?

A new ecosystem of tech-enabled platforms has emerged to simplify the process of setting up and managing SPVs. These platforms offer different strengths and pricing models, catering to various needs, from angel syndicates launching their first deal to professional fund managers requiring institutional-grade administration.

AngelList

A pioneer in the space, AngelList is a US-based platform (Delaware) optimized for venture and angel investing. Its key strength is its vast network of LPs, and it is ideal for syndicate leads focused on tech startups. The platform is known for its speed (~1 week setup) and standardized flat-fee pricing of ~$8,000 per SPV.

Carta

Carta offers a comprehensive, end-to-end fund administration service for professional GPs and established VC firms. It supports both U.S. and international structures (via its acquisition of Vauban) and is designed to handle complex, customized funds that require ongoing administration. Pricing is custom-quoted on an enterprise basis.

Roundtable

Roundtable is a leading European platform specializing in cross-border angel investing. It is ideal for European startup founders, investment clubs and fund managers, with a presence in key jurisdictions like Luxembourg and France. Their pricing is deal-based at 1% of funds raised (with a €5,000 minimum), and they are known for fast setup times and their social community approach.

bunch

bunch is a Germany-based, all-in-one private markets platform designed for professional fund managers with cross-border European investments. It provides a full suite of digital tools to handle the complexity of European regulations. Pricing is on a custom, enterprise model tailored to the fund's specific needs.

Allocations

Allocations, a U.S. platform (Delaware), markets itself on speed and simplicity, claiming to be one of the fastest ways to launch an SPV. It is designed for rapid deal execution, making it a good fit for frequent syndicators who prioritize speed. It has a premium pricing model, with a standard SPV starting at ~$10,000.

Sydecar

Sydecar is a U.S.-based (Delaware) platform focused on providing a low-cost, automated solution. With a pricing model that starts with a minimum fee of ~$4,500, it is ideal for cost-sensitive new managers and those executing smaller deals where higher fees would be prohibitive.

Flow (Apex)

Now part of the global Apex Group, Flow is an institutional-grade platform primarily focused on the U.S. market. It is designed to provide a high-touch experience for larger SPVs and funds with many LPs. Pricing is on a custom, enterprise basis, reflecting its institutional focus.

Odin

Odin is a UK-based platform focused on serving angel syndicates in Europe. It offers a fast, deal-based fee structure and also supports the creation of fund feeder vehicles for pooling investors into larger VC funds.

Securitize

Securitize is a more recent arrival, focused on asset tokenization, not a traditional SPV setup platform. Its core product is on creating tokenized securities to enable fractional ownership and provide liquidity via its own secondary trading market (ATS). The process is longer (1-3+ months) and pricing is higher and custom-quoted due to its complexity.

SPV Provider Comparison Table

What’s next for SPVs: future trends

The Special Purpose Vehicle is not a static tool; it is continuously evolving to meet new market demands and technological possibilities. Key emerging trends suggest a future where SPVs become more technologically integrated, purpose-driven, and standardized, all while navigating increasing demands for transparency.

- Tokenization and digital securities: An emerging trend is representing SPV ownership interests as digital tokens on a blockchain or building on Web3 architecture. This could significantly increase liquidity and efficiency in secondary markets, combining the legal certainty of an SPV with the technological benefits of blockchain.

- DAOs as investment vehicles: Decentralized Autonomous Organizations (DAOs) are emerging as a potential new way to organize and manage control within an SPV, with providers investing in new blockchain products to deliver the service.

- ESG and impact-driven SPVs: There is a growing use of SPVs for specific sustainable or social goals. This includes creating "Green Bonds" by securitizing assets like solar leases, or "Social Impact Bonds" that fund social programs with investor returns tied to successful outcomes, making green projects faster to fund and simpler to invest in.

- Automation and AI management: Technology is being integrated into SPV operations. Algorithms could soon automate complex cash flow management and compliance monitoring, while AI may one day optimize financial decisions, potentially reducing costs and human error.

- Standardization and Simplification To counteract complexity, a trend is emerging towards standardizing SPV documentation. This includes using pre-established "utility" SPVs or "shelf companies" that allow for faster and more cost-effective setup for new deals.

Conclusion

For investors and syndicate leads looking to safeguard and separate investments, SPVs offer a flexible, transparent, and cost-effective way to pool capital.

With no ongoing fund commitments, SPVs allow participants to invest on a deal-by-deal basis while simplifying cap table management for founders.

Roundtable’s platform makes SPV formation and management simple – streamlining onboarding, compliance, investor reporting, and ongoing administration.

- Simple set up: From entity formation to bank account opening, Roundtable handles every step of your SPV launch.

- Tailored legal documents: Access professionally drafted subscription agreements and operating documents aligned with your specific deal terms.

- Compliance built-in: KYC, AML, and investor onboarding are fully integrated for a seamless investor experience.

- Cost-effective solutions: Our platform minimizes setup costs and back-office complexity, allowing you to focus capital on your investments.

SPV FAQs

How do accounting standards decide if an SPV must be consolidated?

Modern accounting standards (like IFRS 10 and US-GAAP) look past simple voting rights to determine control. You must consolidate an SPV onto your balance sheet if you both direct the activities that most affect its returns and absorb the majority of its variable returns. If not, it can remain off-balance-sheet, but still requires extensive disclosure in your financial notes.

What features are essential for a truly bankruptcy-remote SPV?

A truly bankruptcy-remote SPV, standard in jurisdictions like Delaware or Luxembourg, requires several non-negotiable features that rating agencies review first:

- Independent governance: At least one independent director empowered to block any voluntary insolvency filing.

- Limited-purpose charter: Prohibits any activities outside the defined transaction to prevent unforeseen liabilities.

- Separateness covenants: Requires separate bank accounts, books, and a strict prohibition on commingling cash with the sponsor.

- Contractual protections: "Non-petition" and "limited-recourse" clauses in every contract to prevent creditors from forcing bankruptcy.

How long does it take to set up an SPV?

A simple, turn-key SPV can be incorporated in 2–5 business days. However, the full launch process, including drafting transaction documents, opening bank accounts, and wiring capital, can take 20–30 days. Venture deal SPVs on automated platforms can compress this timeline significantly, often to under 10 days.

What ongoing governance tasks should be expected?

Even passive SPVs require ongoing management. Key tasks include calculating cash flow waterfalls for investor payments, holding director meetings to certify covenant compliance, and coordinating annual audited financial statements. A professional administrator usually bundles these tasks into a fixed annual fee so the sponsor can focus on asset performance.

How does an SPV differ from a SPAC or a regular subsidiary?

These entities serve very different purposes. A regular subsidiary is used for ordinary, ongoing business operations and is always consolidated. A SPAC is a publicly-funded shell company created to find and acquire an unknown future target. An SPV is used to isolate the risks and assets of a known, defined project or asset set.

Can the shares or notes of an SPV be tokenized?

Yes, SPV securities can be issued as digital tokens on a blockchain, as demonstrated by recent institutional funds. This does not waive securities law or AML compliance; the same legal paperwork and investor checks are required. The primary benefit is improved efficiency and liquidity in secondary markets, though it may come with higher initial legal spend and evolving regulatory guidance.

{{learn_banner}}